[S#1] D) Yield Curve Inversions 2.0: Near Term Forward Spread

Index:

Series#1: How Macroeconomic Factors of SPY Impact Your Trading

D) Yield Curve Inversions 2.0

Key Takeaways:

The Near-Term Forward Spread (NTFS) measures market expectations for near-term conventional monetary policy rates

NTFS = 3-month Treasury bill rate, 18 months from now minus the current 3-month rate

If the spread is negative, there is an expectation that the Federal Reserve will have to reduce rates because the economy slows down too much

Therefore, it can be a very good predictor of a recession and typically happens in late slow growth periods of the economy

It has been verified that the Federal Reserve (in a blog post and press conferences) look at this spread when making decisions about the economy

Similar to my conclusion in my first post about yield curves, for long-biased momentum swing traders and in general, retail investors when the NTFS changes in a strong direction (positive to negative, or negative to positive), you will want to keep an eye out for market downturns or further signs of market weakness.

This will be a rather short post but I believe a good addition to my original post on yield curve inversions.

![[S#1] D) Significance of Yield Curve Inversions](https://substackcdn.com/image/fetch/$s_!YCc0!,w_140,h_140,c_fill,f_webp,q_auto:good,fl_progressive:steep,g_auto/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F97667a59-382f-4c33-b31e-3c67e2a30fe5_1024x1024.png)

Because of how long the original post was I wanted to break out this part into a small iteration of the first.

Now all those curves and graphs and spreads are all fine and dandy, but I forgot to mention a pretty recently famous and useful spread!

The Near-Term Forward Spread

f₁₈,₃ - 3m

For most retail traders this, “f₁₈,₃” will be new to you. This is a forward rate. It is a 3-month Treasury bill rate, 18 months from now. To read this, the first subscript is “when”, and the second is “what”. So it can be thought of as f ᵥᵥₕₑₙ, ᵥᵥₕₐₜ. The spread is the forward 3-month rate (in 18 months) minus the current 3-month rate. It is a forward money market yield minus the current money market yield.

This spread can be interpreted as a measure of market expectations for near-term conventional monetary policy rates. Its predictive power suggests that when market participants have expected—and priced in—a monetary policy easing over the subsequent year and a half, a recession was likely to follow. The near-term spread also has predicted four-quarter GDP growth with greater accuracy than survey consensus forecasts, and it has substantial predictive power for stock returns.

In the research paper (referenced below), they conclude that the near-term forward spread subsumes essentially all of the information in other popular measures of term spreads when it comes to forecasting recessions and GDP growth.

To interpret this spread it is stated that when the near-term forward spread is negative, it is signaling that investors expect the Federal Reserve to ease monetary policy over the specified horizon.

Because there is a belief that the future rate (3-m forward rate, 18-m from now) will be less than the current 3-m T-bill rate.

f₁₈,₃ < 3 months = Negative Spread

The research paper explains in better detail below as they state:

When do investors expect monetary policy easing [lower short-term interest rates]? Presumably, when they anticipate a substantial slowing or decline in economic activity. Consequently, if market participants have some foresight, a quite logical result is that low readings for the near-term forward spread will tend to precede (and thus can be used statistically to forecast) recessions. This interpretation implies that inversions of the near-term forward spread do not cause recessions. Rather, they reflect something that market analysts already track closely—namely, investors’ expectations for monetary policy over the next several quarters and, by extension, the economic conditions driving those expectations. Although long-term spreads also incorporate this information, they are likely to be affected by other factors that are unimportant for forecasting recessions, which degrades their forecasting power.

To Manually Calculate this Spread:

This link will bring you to a tool made by, Chatham Financial that displays Treasury Forward Curves. From here you would use the current date 3-month rate SOFR and subtract it from the same rate but 18 months in the future.

Therefore [f₁₈,₃ - 3 months] = 3.93 - 5.3 = ~ -1.37%

Automatic Calculation and Visual

I was only able to find one site that actually does this calculation automatically and charts the data, which is delayed slightly but still a good tool as it gives a good visual and interactive experience with it (Near Term Forward Spread Tool).

Digging Deeper

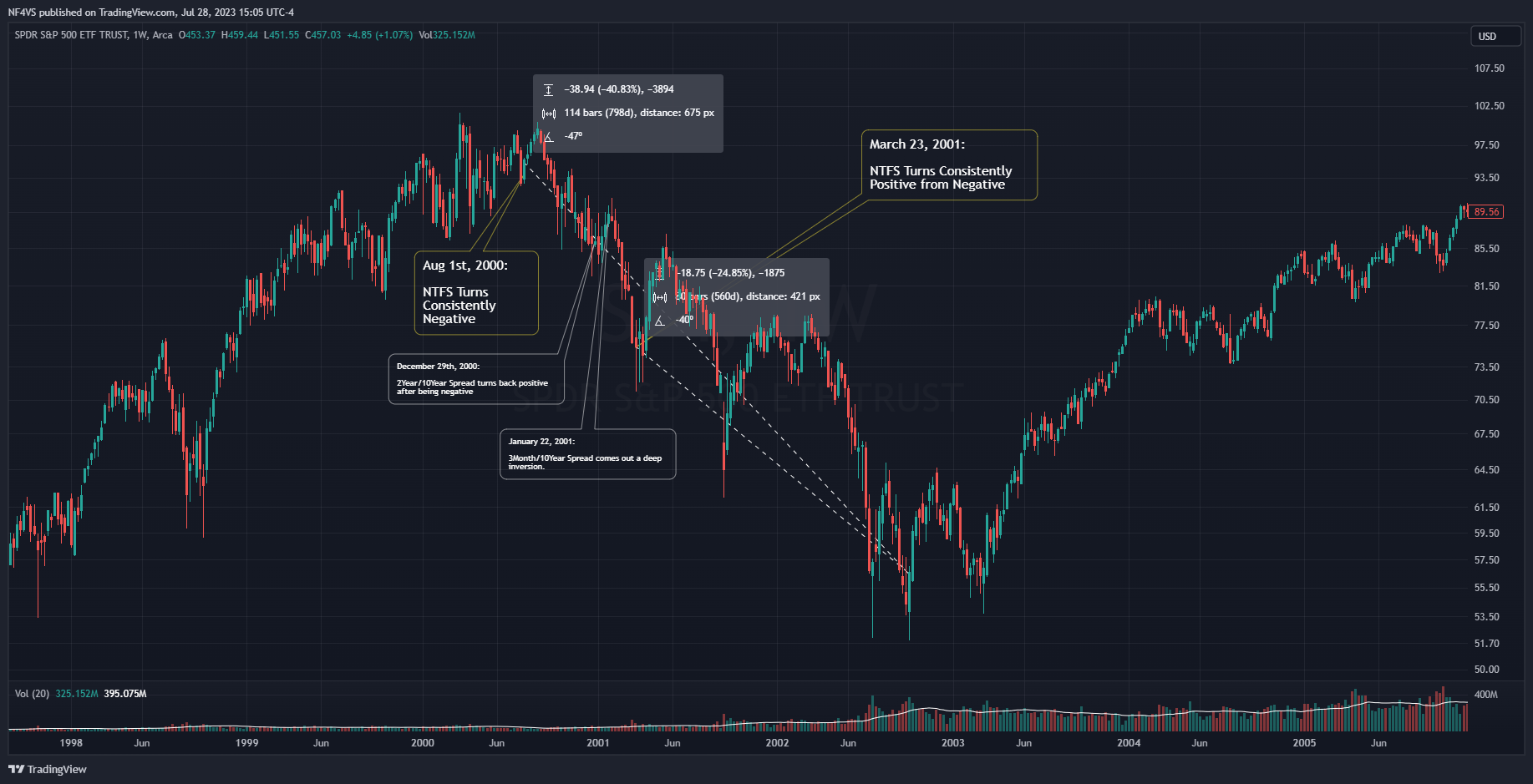

2000s Recession (Fed approximates recession on March 2001)

NTFS Turns Consistently Negative - Aug 1st, 2000

NTFS Turns Consistently Positive from Negative - March 23, 2001

For the 2000/01 recession, soon after the spread turned negative, SPY started to fall.

2007/08 Recession (Fed approximates recession on Dec 2007)

NTFS Turns Consistently Negative - July 19th, 2006

NTFS Turns Positive for ~46 days Starting - May 30th, 2007

NTFS flips negative to positive many times

NTFS Turns Consistently Positive from Negative - March 4th, 2008

From the recession of 2007/08, after the spread turned negative, SPY still ran up before eventually switching back to positive for roughly a month. This is when things took a turn for the worst.

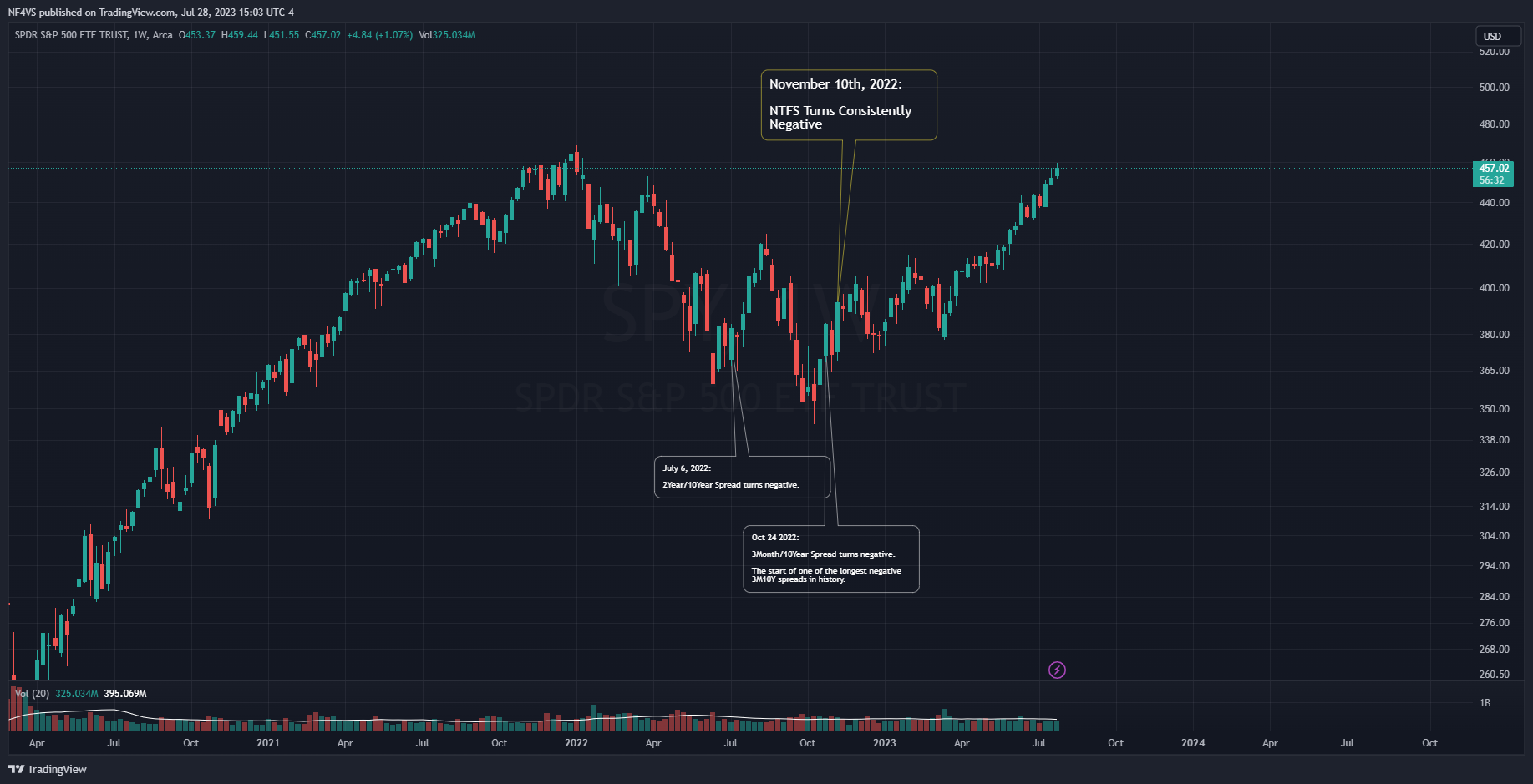

Current Economy

NTFS Turns Consistently Negative - November 10th, 2022

NFTS Remains Negative as of Writing - July 28th, 2023

We have entered the negative spread territory for quite some time now as markets continue to persist. SPY and other index ETFs are looking very close to hitting record all-time highs. I believe soon, things will start to topple. When that is? I am not sure, but keeping tabs on the NTFS is probably a good idea.

Conclusion

For a couple of finger waggers who will say, “This is silly, the spread went negative and positive multiple times and did not cause a recession”. I need you to revert back to my original post. I would also need to point out something that was stated above, that the interpretation of this negative spread implies that inversions of the NTFS do not cause recessions. It is that it has good predictive power.

This DOESN’T mean this is a one-stop shop answer to predicting when or if a recession will happen. Again, this should be a tool that retail investors can use to gain a better understanding of the macro landscape and how it could potentially impact the general markets (ie. SPY 0.00%↑ or QQQ 0.00%↑).

Similar to my conclusion in my first post about yield curves, for long-biased momentum swing traders and in general, retail investors when the NTFS changes in a strong direction (positive to negative, or negative to positive), you will want to keep an eye out for market downturns or further signs of market weakness.

References:

Understanding the Market Outlook - Interest Rate Tutorial - This information comes directly from a video that Mark Meldrum (an investor/professor/CFA instructor) published a while back.

Research Papers:

The Near-Term Forward Yield Spread as a Leading Indicator: A Less Distorted Mirror - A paper on the Fed’s site about this spread and its effectiveness

Tools:

Term SOFR, Fallback Rate (SOFR), and Treasury Forward Curves - Used to manually calculate the Near Term Forward Spread

Near Term Forward Spread Tool - Visual interpretation of the NTFS